Are You Saving Enough Money To Retire On Time?

When do you want to retire? Maybe a “soft-retirement” into part-time consulting at 50? Or a more traditional 65, or maybe even 70-ish if you love your work.

My guess is that you already have a retirement bucket list and are dreaming about reaching this milestone. But a dream isn’t going to get you anywhere in the real world if you don’t put some muscle behind it. Have you crunched the numbers and figured out how much you need to save to retire when you want to? (*hint: Try our online tool right here).

According to the Employee Benefit Research Institute’s (EBRI) 2016 retirement confidence survey, 77% of workers polled said they expect to retire at a later age than they previously planned, and all of their reasons had to do with uncertainty regarding finances.¹ Don’t let this be your story too.

Educate Yourself

According to the same EBRI study, 48% of workers have never calculated how much they will need to live the way they want to when they retire.² I hate to break it to you, but you can’t expect a leprechaun to show up at your door with a pot of gold. (My daughter is obsessed with leprechaun's, so I had to sneak one in here). You have to do your part if you want to get where you want to be.

It’s simple. If you don’t know how much you need, how will you know how much to save to create a realistic retirement plan? The complicated part is that figuring out your savings goals isn’t as easy as plugging some data into an online calculator and planning your life around the results. It takes real work. You need to create a real financial plan, organize your investments, create an investment plan, optimize your 401k plan at work, and actually execute it all.

Everyone has their own unique set of factors to consider. You’ve got current savings amounts, years from retirement, the overall stability (or instability) of your career, the economy, and how you want to live in retirement. Ballpark figures aren’t going to help you here.

So you nix the calculators, but advice from financial professionals can be vague too. Most of them will tell you to save 10-20% of income towards retirement. Why doesn’t that work?

First of all, depending on your income, 10% vs. 20% is a massive difference.

Second, your age needs to be considered. If you start saving in your 20s, 10% might serve you well due to compound interest, but if you are getting a later start, you will need to save more. So if calculators and general advice won’t help you, what do you do?

Understand Benchmarks

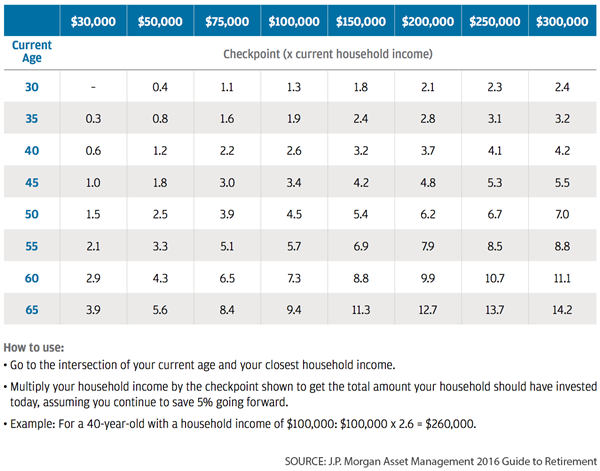

While charts and calculators won’t speak to your personal situation, they can give you an idea of what your savings should look like right now if you want to meet your goals in the future.

Take a glance at the chart below. Instead of showing you what you should save monthly from here on out until retirement, it lets you know if you are on track by looking at what you have saved up to this point. From there, you can figure out how to catch up if you find yourself lagging behind.

Using a benchmark like this one gives you a better idea of your progress because it looks at your current circumstances. Here’s an example: many of us plan to rely on Social Security or pensions to provide the bulk of our retirement income. But there’s a catch! The more you earn, the less Social Security you will receive, so what you need to save to retire on time will change based on your pre-retirement income.

Maximize It

You can’t predict every aspect of your retirement financials, but one thing you can control is how much you save. Social Security may change, inflation will increase living expenses, medical costs are unpredictable, and what the economy will do is anyone’s guess. But if you consistently save as much as you can, you won’t regret it.

If you feel like your budget can’t handle anything extra, make it a habit to save any surprise money that comes your way, whether it’s a bonus from your employer, an increase in pay, or a tax refund.

A Handy Rule-of-Thumb 25:1

If you remember one ratio from this blog post, remember 25:1. For every dollar of shortage between your Social Security and/or pensions and your retirement living expenses, you need 25x that in savings. That’s not a mistype. It’s really 25x. Let’s do a quick example. If your numbers show that your retirement expenses will be $20,000 a year more than is coming in from outside sources, you will need a whopping $500,000 in savings.

I like this ratio not only because it’s easy to remember, but also because it highlights how capital intensive — how much money you need to save — to fund your retirement.

Reassess Regularly

Life happens faster than we want it to (and tons of crazy shit happens along the way). Once you’ve set your goals and calculated how much you need to save, make it a habit to reevaluate once a year to make sure you are still on track to meet your benchmarks.

It also doesn’t hurt to check back in if you go through any life transitions like a job change, marriage, divorce, or the birth of a child.